Edge+

Advanced Solvency II capabilities with full standard model calculations, customizable parameters, and comprehensive reporting

Key Features

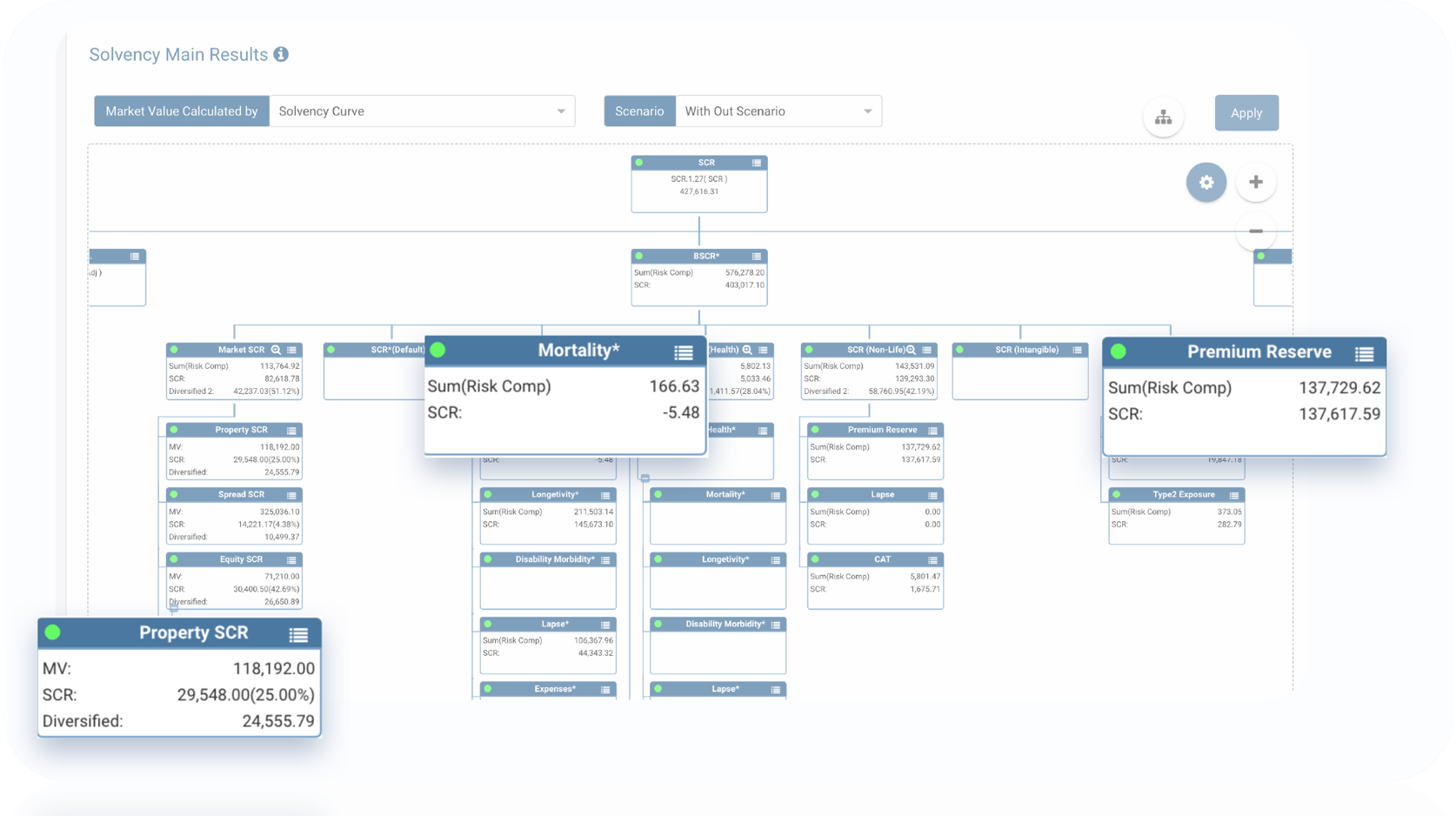

Full, controlled calculation of the Solvency II standard model: SCR by sub-module via the BSCR matrix, what-if asset simulation, and outcome comparison with narration.

Interest rate, equity, and spread risk alongside currency, concentration, and property risk, aggregated through the correlation matrix.

Smith-Wilson curve fitting, symmetric adjustment, and counterparty and actuarial risks, calculated automatically and consistently.

End-to-end EBS management with capital projection and full control of assumptions.

Regulatory template generation with helper-tab automation and an auditable output trail. All reports downloadable to Excel.

Forward solvency ratios with stress-conditioned projection, ready for Board and ORSA narratives.

Solvency II Standard Model

Enjoy a full and controlled calculation of Solvency II standard model that automatically determines asset solvency avenues and enables manual updating. Edge+ offers complete control of Solvency parameters and bottom-up SCR calculations.

Bottom-up calculations for all major risk categories:

- Equity (with SA separation)

- Spread risk

- Interest rates (including liabilities effect)

- Currency risk

- Property risk

- Concentration risk

- • Automatic asset solvency determination

- • Manual parameter updating capabilities

- • Complete correlation matrix control

- • Financial scenario applications

Economic Balance Sheet, Projection & Reporting

From the economic balance sheet through forward-looking capital projection to regulatory QRT reporting, automated end to end.

- EBS management

- Capital projection

- Full control of assumptions

- Forward solvency ratios

- Stress-conditioned projection

- Board & ORSA narratives

- Smith-Wilson curve fitting

- Symmetric adjustment

- Counterparty & actuarial risks

- Regulatory template generation

- Helper-tab automation

- Auditable output trail

Full Control & Flexibility

- Full control of Solvency parameters

- Customizable yield curves

- Adjustable correlation matrices

- Bottom-up SCR calculations

- Financial scenario applications

- Excess yield assessment tools

Apply financial scenarios to reevaluate impact on SCR and assess excess yield in relation to capital requirements.

- Filter data with multiple segments

- Drill down to asset/policy level

- Custom results and analytics

- Slice and dice data like Excel

- Visualize any report easily

- Compare through historical portfolios

Reporting Excellence

All reports are downloadable to Excel for seamless integration with your workflow. Get RemitRix Edge+ with RemitRix Horizon to enjoy automatic reporting – QRT filing with main calculations file and helper tabs.

On-demand technical support is offered through an easy-to-use web-based ticketing system. Get help when you need it.

Let's Get Started

Partner with us to transform your Solvency II risk management